Expands Exclusive Partnership With PhonePe")

Expands Vehicle Service")

Economic Times held out a report that Insurance corporations can begin with a low capital base of Rs.50crore as a part of a spate of reforms set in movement. Several specialists warned that insurance being a danger umbrella, low capital base might result in buyer insecurity. 20-21 Annual Report of the Insurance Regulatory Development Authority of India (IRDAI) says: “The pandemic has cemented positive paradigm shifts for insurance. Higher risk awareness and acceleration in digitization are positive structural trends for insurance.” This article intends to clarify a few of the phrases used in the insurance sector and the chance elements in the insurance sector and the methods to deal with them in the pursuits of each the establishments, people, and enterprises.

Definitions

It is vital to grasp the way in which the important thing gamers are outlined. Insurance is a way of defending people, enterprises, and corporates in opposition to the chance of shedding property or worth of property contingent on generally undefinable uncertainties. An entity which supplies insurance is called an insurer, insurance firm, or insurance provider. An individual or entity who buys insurance is called an insured or policyholder. A broking agency licensed and controlled by the Insurance Regulatory Development Authority of India (IRDAI) acts as an middleman between the insured and insurer. Many a time, the insured is unaware of the explanations for insuring himself or his agency, the methods in which (s)he or her or his agency is protected and the way in which claims are responded to when the necessity arose. Agents are those that work on behalf of the Insurance Companies to canvas the insurance policies explaining absolutely the implications of such insurance policies and the advantages of insurance by paying a small premium to cowl a big unknown danger.

“Insurance penetration and density are two metrics, among others, often used to assess the level of development of the insurance sector in a country. While insurance penetration is measured as the percentage of insurance premium to GDP, insurance density is calculated as the ratio of premium to population (per capita premium).”

Underwriting in Insurance:

According to Investopedia, “insurance underwriters are professionals who consider and analyse the dangers concerned in insuring individuals and property. Insurance underwriters set up pricing for accepted insurable dangers. The time period underwriting means receiving remuneration for the willingness to pay a possible danger. Underwriters use specialised software program and actuarial information to find out the chance and magnitude of a danger.

Insurance underwriters assume the chance concerned in a contract with a person or entity. For instance, an underwriter could assume the chance of the price of a fireplace in a house in return for a premium or a month-to-month fee. Evaluating an insurer’s danger earlier than the coverage interval and on the time of renewal is an important perform of an underwriter.”

Surveyors/Assessors: When the insured studies lack of an insured asset, the insurer engages a Surveyor/Assessor to judge the loss and the sustainability of the declare in phrases of the coverage issued by the insurer.

All the insurance insurance policies carry a positive print – largely unreadable simply.

Understanding the clauses of the coverage is invariably troublesome and interpretation is all the time to the benefit of the insurer greater than the insured. The positive print carries the dangers that the insurer is prone to compensate when sure happenings trigger the chance. The Policy is the contract between the insurer and the insured whereby the insured is obligated to pay the premium frequently to maintain the coverage present always. A declare in opposition to the coverage is sustainable solely when the situations included and ipso facto agreed to by the insured are absolutely honoured.

According to the Annual Report of IRDAI, insurance penetration in India elevated from 3.76 per cent in 2019-20 to 4.20 per cent in 2020-21, registering a development of 11.70 per cent, whereas the primary decade of insurance sector liberalization witnessed the rise in penetration from 2.71 % to five.20 %. . During the primary decade of insurance sector liberalization (2000-2010), the sector has reported enhance in insurance penetration from 2.71 per cent in 2001- 02 to five.20 per cent in 2009-10. Thereafter, it declined for 5 years to register once more a rise to the present stage of 4.20 %.

Insurance density relies upon upon the individuals’s notion of the dangers that want insurance for sure and regularity in fee of premium dedicated by them for the intervals specified in the coverage. In India, insurance density is reported to be constant at round Rs.500 throughout 2019-21.

Life is insured beneath a life insurance coverage whereas the home, tools, utilities are insured beneath normal insurance. There are variety of methods in which premium is calculated and the actuaries assess the dangers inherent in a selected exercise – life, well being, vehicles, devices, equipment and so on., and the bigger the variety of insured, the decrease the premium may very well be. Technology developments have made life simpler for the insurance corporations in the calculation of premium, assessments of loss and settlement of claims.

Risk Management in Insurance:

Risk is totally different from uncertainty. In the case of danger, we all know the likelihood of its prevalence however not the time at which it happens and what loss it’s going to entail for the holder. I’ll cite a few examples.

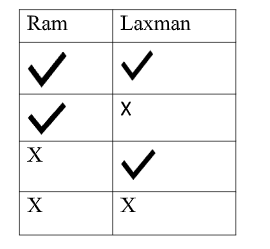

• Example 1: Ram and Laxman are two brothers, who may very well be both sick or wholesome. Thus, there are 4 prospects.

Each has a 25 % risk of prevalence. The danger of assault of illness can come from a lot of sources and at various occasions and with various depth. There is a risk of both or each popping out of illness once more at totally different occasions with totally different outcomes post-sickness. Therefore, we have no idea whether or not it’ll occur, when it’ll occur and the way it will occur and with what monetary penalties.

Types of Risk:

• Covariant dangers: have an effect on massive numbers of individuals on the similar time, e.g. epidemics, the delta variants of the Covid-19 and so on.

• Idiosyncratic dangers: have an effect on a small section of the inhabitants

• Minor and main dangers: Minor dangers could also be resolved with mere session whereas main dangers require hospitalization with excessive prices. Some main dangers just like the one not too long ago confronted universally throughout the globe with totally different intensities require enormous investments in infrastructure for creating and well timed distribution of vaccines.

• Catastrophic dangers: have an effect on a big section of the inhabitants and have excessive unit prices, e.g., Covid-19.

Sources of Risk

Just a few examples

Natural: flood, drought

Health: sickness, epidemic

Lifecycle: start, outdated age, loss of life

Social: crime, warfare

Economic: unemployment, monetary disaster, recession

Political: riot, coup d’état, fall of elected democracies with

majority shifts in political events’ alignments

Environment: air pollution, nuclear catastrophe

Social safety covers well being and life-cycle dangers, and a few financial dangers like unemployment. The penalties of such dangers can have an effect on people, households, tribes, communities, space, nation, or a gaggle of countries. Each consequence has a worth to pay. Not all of the dangers are insurable. Risks on land are totally different from these occurring in air or sea. Airborne and Marine dangers are often coated by exporters and importers whereas participating in monetary transactions by lending establishments.

There are six normal necessities of an insurable danger:

1. Large variety of publicity models

2. Accidental and unintentional loss

3. Determinable and measureable loss

4. No catastrophic loss

5. Calculable probability of loss

6. Economically possible premium

Insurance helps in sustaining financial stability, assures monetary compensation for the cognizable losses incurred, promotes business actions, enhances financial savings and funding, and strengthens employment alternatives by security nets both by the governments or specialised establishments. Risk administration has a couple of important actions: danger identification, quantification/measurement, mitigation, and coping mechanisms. Quantitative danger evaluation entails numerical evaluation of the likelihood of every danger by both Monte Carlo methodology or Decision Tree mentioning the possibilities and selections and Expected financial worth methodology (EMV).

In our lives, dangers are prevalent in each exercise – whether or not it’s deciding on a partner or a business accomplice, whether or not it’s deciding on a product or course of for manufacturing, the place to promote to the way to promote and the pricing of the product. From close to neighbours to abroad, from governments to non-public collaborators and establishments to the selection of a lender, there are dangers. Some dangers as talked about in this text are insurable whereas many are resolved by software of frequent sense or instinct. We had an extended journey of regulated insurance mechanism. From the variability and nature of dangers, insurance corporations train their limitations of protection throughout the regulatory framework. When rules are put to emphasize, their potential to assist the shoppers will come up for check. In a dynamic world, change is fixed. Any regulatory change can’t be completed in the icy chambers of a regulator. They should be completed by elaborate session with all of the stakeholders and transparently.

Disclaimer

Views expressed above are the writer’s personal.

END OF ARTICLE

{kind=link}